The Bond counsel are paid a significant sum of money to accurately state the law in the bond prospectus – a critical document that investors rely upon when they spend millions of dollars.

In all the bonds issued by the Fossil Ridge Metro District 3 (Solterra), Brookfield, who controlled the Boards when the Bonds were issued all stated the same facts.

And investors paid $29 million to Fossil Ridge Metro District and the District wrote Brookfield checks for $29 million based upon what the lawyers and Brookfield said in the bonds:

From the last bond – 2016 – here is what the Bond lawyers said the law required:

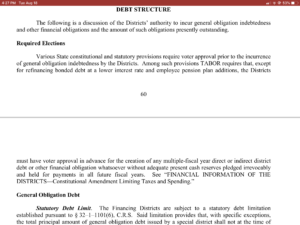

“Required Elections

Various State constitutional and statutory provisions require voter approval prior to the incurrence of general obligation indebtedness by the Districts. Among such provisions TABOR requires that, except for refinancing bonded debt at a lower interest rate and employee pension plan additions, the Districts must have voter approval in advance for the creation of any multiple-fiscal year direct or indirect district debt or other financial obligation whatsoever without adequate present cash reserves pledged irrevocably and held for payments in all future fiscal years.” 2016 Bond Issue, p. 60 (Emphasis added)

The lawyers said – before these bonds can issue, as required by the constitution for the state of Colorado – THE VOTERS MUST VOTE TO APPROVE ISSUING THE BONDS AND GOING INTO DEBT.

THE VOTERS MUST REALLY WANT TO DO THIS – SO MUCH SO THAT THEY WILL CAST THEIR VOTE TO ISSUE NEW BONDS AT A PUBLIC ELECTION.

Now, here is the Brookfield Omission – not about the law – but about the facts. Here is what Brookfield said in all the bonds:

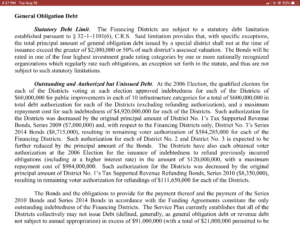

“Outstanding and Authorized but Unissued Debt.

At the 2006 Election, the qualified electors for each of the Districts voting at such election approved indebtedness for each of the Districts of $60,000,000 for public improvements in each of 10 infrastructure categories for a total of $600,000,000 in total debt authorization for each of the Districts (excluding refunding authorization), and a maximum repayment cost for such indebtedness of $4,920,000,000 for each of the Districts.” 2016 Bond Issue, p. 61 (emphasis added)

BROOKFIELD NEVER TOLD THE INVESTORS IN THIS CRITICAL PORTION OF THE BONDS THAT THE “QUALIFIED ELECTORS” (VOTERS) WHO WERE SO EXCITED AND ENTHUSIASTIC ABOUT GOING INTO ALL THIS DEBT . . . . WOULD NEVER HAVE TO PAY A DIME BECAUSE THOSE “QUALIFIED ELECTORS” WERE

8 EMPLOYEES

OF BROOKFIELD

WHO DID NOT LIVE HERE, DID NOT PAY TAXES HERE, AND NEVER WOULD

WHO HAD A CONFLICT OF INTEREST WITH THE ACTUAL PEOPLE WHO WOULD PAY THE TAXES

8 EMPLOYEES OF BROOKFIELD WHO COULD NEVER REPRESENT THE INTERESTS OF THE ACTUAL SOLTERRA RESIDENTS.

This material misrepresentation of the facts by omitting this material information in each of the Fossil Ridge Metro District bonds is wrong. They are not telling the full story.

The only way to say in this critical legal document that the voters of the Districts actually voted to approve issuing the new $10 million bond – and payment to Brookfield – is to ACTUALLY HAVE AN ELECTION WHERE THE ACTUAL 2000+ VOTERS IN SOLTERRA ACTUALLY VOTE TO APPROVE THE BOND

In every bond document, Brookfield materially misled the bond investors by indicating real Solterra voters who actually lived here and paid the taxes approved issuing these bonds – when in fact it was 8 employees of Brookfield who never lived here and never paid any of the taxes they imposed on the future residents.

What will the Solterra Board say in 2020. Will they continue the Brookfield Omission and embrace this material misrepresentation violating their fiduciary duty to the residents and the investors.

Or will they restore the residents’ right to vote, have an actual election and follow the law which states the bonds cannot issue unless the voters – the real voters – vote to approve the bonds at a public election. Here is the law again – as stated in the 2016 bond. A public election is “required“

“Required Elections

Various State constitutional and statutory provisions require voter approval prior to the incurrence of general obligation indebtedness by the Districts. Among such provisions TABOR requires that, except for refinancing bonded debt at a lower interest rate and employee pension plan additions, the Districts must have voter approval in advance for the creation of any multiple-fiscal year direct or indirect district debt or other financial obligation whatsoever without adequate present cash reserves pledged irrevocably and held for payments in all future fiscal years.” 2016 Bond Issue, p. 60 (Emphasis added)

Mr. Waterman, Mr. Mcgraw, Mr. Brown, Mr. Michelsen, Mr. Hochstein, Mr. Larson, Mr. Wilson, Mr. Dominic, Mr. McCleary, Mr. Plumhoof . . . .

What is your answer. Go along to get along with the Brookfield Omission. Or tell the truth.

John Henderson

Here is the 2016 bond

And the ballot issue where the 8 employees of Brookfield voted as “Qualified Electors”

First and Only Election Certificate of Election Results, 2006-11-07