In yet another anonymous “Solterra Update” issued two days ago, the Solterra Board continues to mislead the residents about the amount of debt and their right to vote on issuing new debt – $10 million to Brookfield plus interest.

Here is a “fact check”, with reference to documents, on the “Solterra Update” issued two days ago, October 13, 2020.

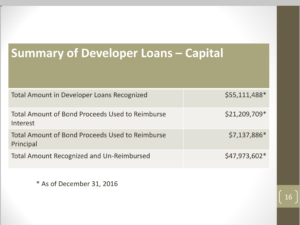

1. What is the total debt. The Board acknowledges that the debt in the Service Plan is $91 million but quickly opines that $21 million of that $91 million is for “Revenue Debt” and “To date, no such Revenue Bonds have been issued and the Districts do not reasonably foresee this category of Revenue Bonds being issued in the future.”

In other words, even though the total “debt” is $91 million, they don’t think Brookfield will ask for $21 million of that debt. This is the same Brookfield that said only $7 million of the $29 million we already paid them went to pay down the “debt” – the rest was interest. That is not a very “prudent” assumption – that Brookfield won’t ask for more money once you open the door.

And that is the real point. Here again is Brookfield’s position in a slide presented to over 200 residents.

The Board is following Brookfield’s instructions and in Brookfield’s world, there is debt and there is interest. The anonymous “Solterra Update” states “Thus, the maximum potential amount payable to Brookfield for District Eligible Costs is $70 million“.

That simply is not accurate.

The $70 million does not include the $21 million interest on the loan and it certainly does not include the interest on the bond debt.

We pay about the same amount in interest as we do principal – so at least double the current $29 million in bond debt we pay and double the total $70/$91 million.

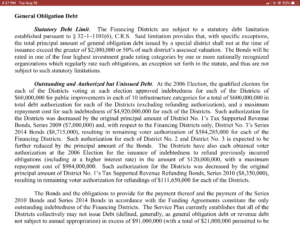

The “maximum potential amount payable”, including interest is at least $140 million and actually much more. According to the ballot issue passed by 8 Brookfield employees in 2006, the maximum is $4.9 billion.

From the 2016 bond prospectus, the total authorized debt limit is $4.9 billion. This is from the “Boards’ own attorneys in 2016.

2. The anonymous “Solterra Update” explains the process for determining “eligible and reasonable costs of improvements“. That is how Brookfield does it – with Brookfield hired engineers and accountants.

That is not consistent with exercising a fiduciary duty. That is not an independent forensic financial audit.

Here, again, is a report on the Brookfield employee who did that analysis “for us”:

There is simply no excuse for not conducting an independent forensic financial audit.

3. “Is a right to vote on bonds legally possible?” They ask the question but never answer it. The answer of course is “yes”.

We can repeal the vote of the 8 Brookfield employees in 2006 just like you can vote on November 3 to repeal the Gallagher Amendment passed in 1982.

The Boards “answer” is a convoluted muddlecock that misleadingly suggests that voting in 2006 to give the board permission to go into debt up to $4.9 billion is the same as voting to issue bonds in the amount of $4.9 billion.

It is not the same of course.

Permission to do something is one vote.

Doing it – issuing bond debt – is a second and independent vote.

The board’s permission to spend up to $4.9 billion voted on in 2006 by 8 Brookfield employees can be reversed before they actually vote to spend $4.9 billion – with a vote just like the Brookfield employee vote 2006 vote and just like your vote on November 3.

For the Solterra Board to work so hard to use the 2006 vote by 8 Brookfield employees to attempt to justify refusing to return our right to vote on tax/bond debt is simply appalling.

4. We published a study showing that we have already paid for the cost of the infrastructure when we paid for our developed lot and bought the homes.

New Research Discloses Brookfield’s Double Billing for Solterra Infrastructure Costs

The Solterra Board responds: it is ok for Brookfield to double charge us for the cost of the infrastructure (once in the money paid for the lot and again, with interest, with the metro district “financing”).

First, they say, “As a ‘for profit’ corporation, Brookfield is entitled to earn a profit on the sale of homes and home sites.”

It is ok, they say, because Brookfield can make as much profit as they want to.

No, they can’t. Not when they are acting as a government and imposing taxes on us without our vote to pay them unaccounted for profits. Governments aren’t allowed to tax to pay profits to themselves – particularly in this case where the government is the developer.

Then, second, the Board says, “this is not about what profit Brookfield may or may not have earned; rather, the question is what District Eligible Costs funded by Brookfield, as defined by the Service Plan, were used to construct public improvements and are eligible for reimbursement to Brookfield.”

In other words, this is about whether the work was done and should be reimbursed.

BUT THE SOLTERRA BOARD STUBBORNLY AND UNREASONABLY REFUSES TO CONSIDER WHETHER OR NOT WE ALREADY PAID THIS BILL.

Residents have always said, if we owe it, we pay it. But we have shown we don’t owe it – we already paid it. It doesn’t matter whether or not they put pipes in the ground – the question is DID WE ALREADY PAY THIS BILL.

5. No one disputes it is a good idea to refinance the $29 million in bond debt Brookfield stuck us with.

But the Solterra Board glaringly fails to justify using all of that savings – $500,000 per year for over 30 years – to pay Brookfield more money.

And they glaringly fail to justify rushing to that decision without having a community conversation about all the other things we could do with that savings – including opposing Brookfield’s claim for any more money.

6. The Solterra Board abuses the executive sessions. That is where all the discussion and decisions occur. Executive sessions should be the exception, not the rule, and the board is prohibited from making decisions except in the public hearings after public discourse, including answering questions – not answering questions after making the decision.

7. According to the costs reported by CRS, the cost of the last election was $30,000.

We have a choice.

We can stop issuing $10 million in new bonds (plus interest) to pay Brookfield more money without a full and independent accounting.

Or we can go along to get along – because as one former appointed board member exclaimed during his losing election campaign – be afraid of Brookfield because they have a lot of money.

This is your money. Hold Brookfield and the Solterra Board accountable before you spend this money. Stop the new debt by signing the recall petitions.

John Henderson